Ukraine’s attacks on Russian oil refineries did not crater the Kremlin’s export earnings overnight—and they were never likely to. So what was their effect, and what should we expect next?

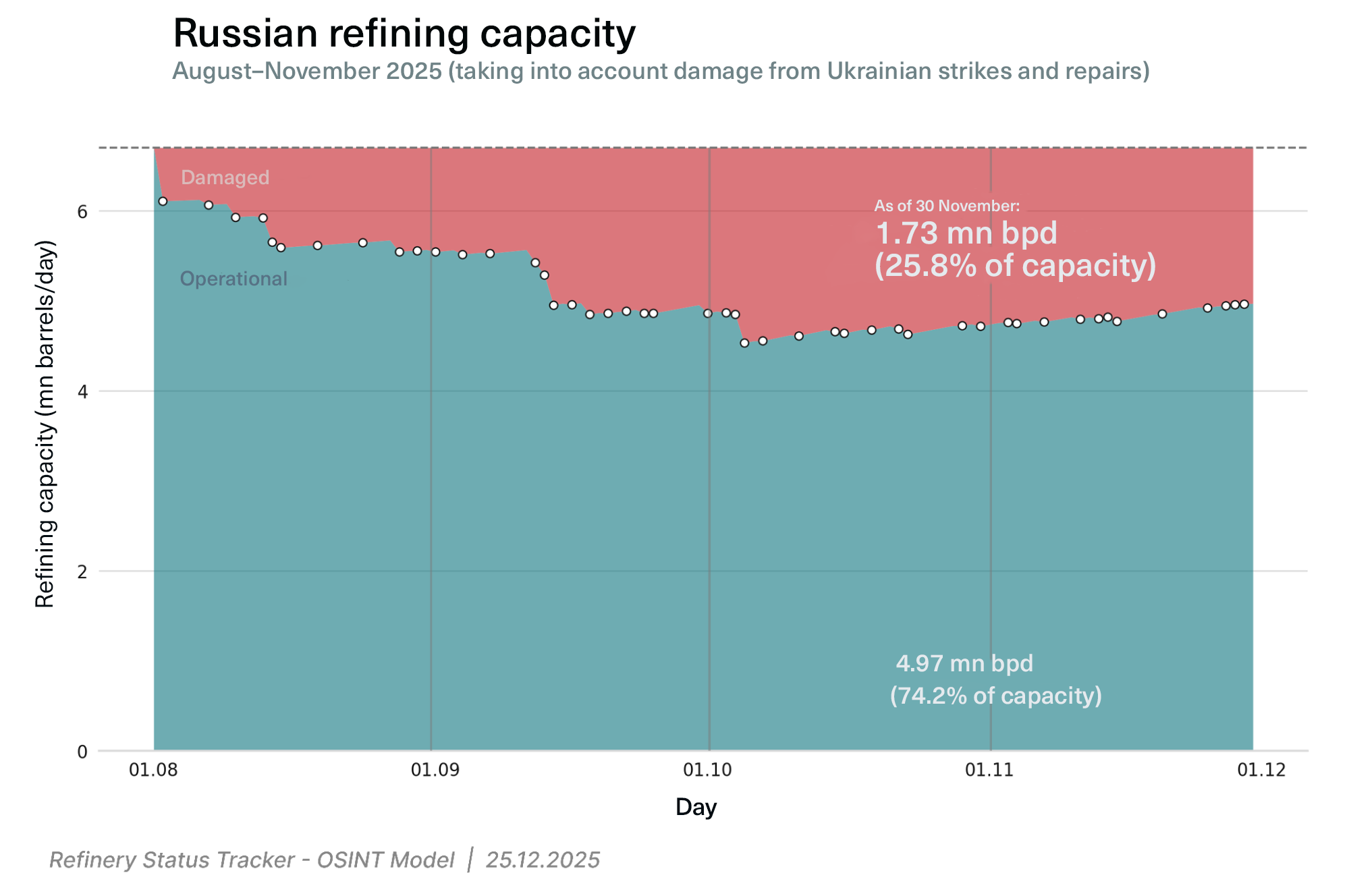

The numbers look paradoxical—Western and Ukrainian media regularly run headlines about the systematic destruction of Russia’s refining infrastructure. Indeed, from August through November 2025, Ukraine carried out more than 60 successful strikes on Russian refineries—an all-time record for the refinery-targeting campaign—knocking out more than 26% of Russia’s refining capacity.

Yet Russia’s overall oil refining volume in 2025 fell by just 1.7%. That calls for calibrated expectations. The real impact of these strikes is visible not in media headlines about burning tanks, but in financial analysts’ spreadsheets—months and years after the attacks. To understand the Ukrainian campaign’s true effect, it makes sense to look separately at the short-term and long-term consequences.

Short-term: why the system holds

Russia’s refining industry is among the largest in the world. As of 2020, the combined nameplate capacity of all Russian refineries stood at about 332 million tons per year, though in practice the country processed roughly 270 million tons. For comparison, the United States’ combined nameplate capacity is about 900 million tons per year—nearly triple Russia’s figure (and U.S. actual throughput is also below nameplate). At the same time, Russia’s domestic consumption of petroleum products is only 110–120 million tons, with the rest exported. This enormous buffer—tens of millions of tons in excess capacity—allows the system to absorb even heavy strikes without collapsing.

The most intense wave of strikes in August–November 2025 hit a range of key Russian refining sites. The Novokuybyshevsk refinery was attacked five times during that period. The Volgograd and Ryazan plants took two to three hits each. The Kirishi, Slavyansk-on-Kuban, Syzran, Astrakhan, and Saratov refineries also sustained serious damage, with operations suspended for periods ranging from two weeks to a month. Large fires and forced shutdowns of primary crude distillation units pushed output at some facilities down by as much as 20% over the period in question.

But these losses were not critical for the sector as a whole, as Russia moved quickly to offset them through spare capacity and accelerated repairs. When a Ukrainian drone hits the Ryazan refinery, Russian dispatchers simply reroute volumes—for example, to the Omsk or Angarsk plants. That is why the fuel shortages in October–November, when filling stations nationwide reported supply disruptions, reflected logistical adaptation rather than systemic collapse. In response, the authorities banned petroleum product exports through February 2026—without disrupting the industry’s overall functioning.

The strikes affected petroleum product exports in a similar way. In September 2025, Russia’s revenues from seaborne exports of petroleum products fell by 13% month on month, while physical volumes declined by 9%. According to the International Energy Agency, Russia’s overall supplies of petroleum products to global markets fell from 315,000 to 250,000 tons per day (7.9%) between January 2025 and December 2026.

These figures look dramatic—but they are not catastrophic for the Russian economy. Moscow partially offset the drop in petroleum product revenues by increasing crude exports (from 4.2 million barrels in September to 4.4 million in October), keeping total hard-currency inflows at an acceptable level.

Long-term: invisible erosion

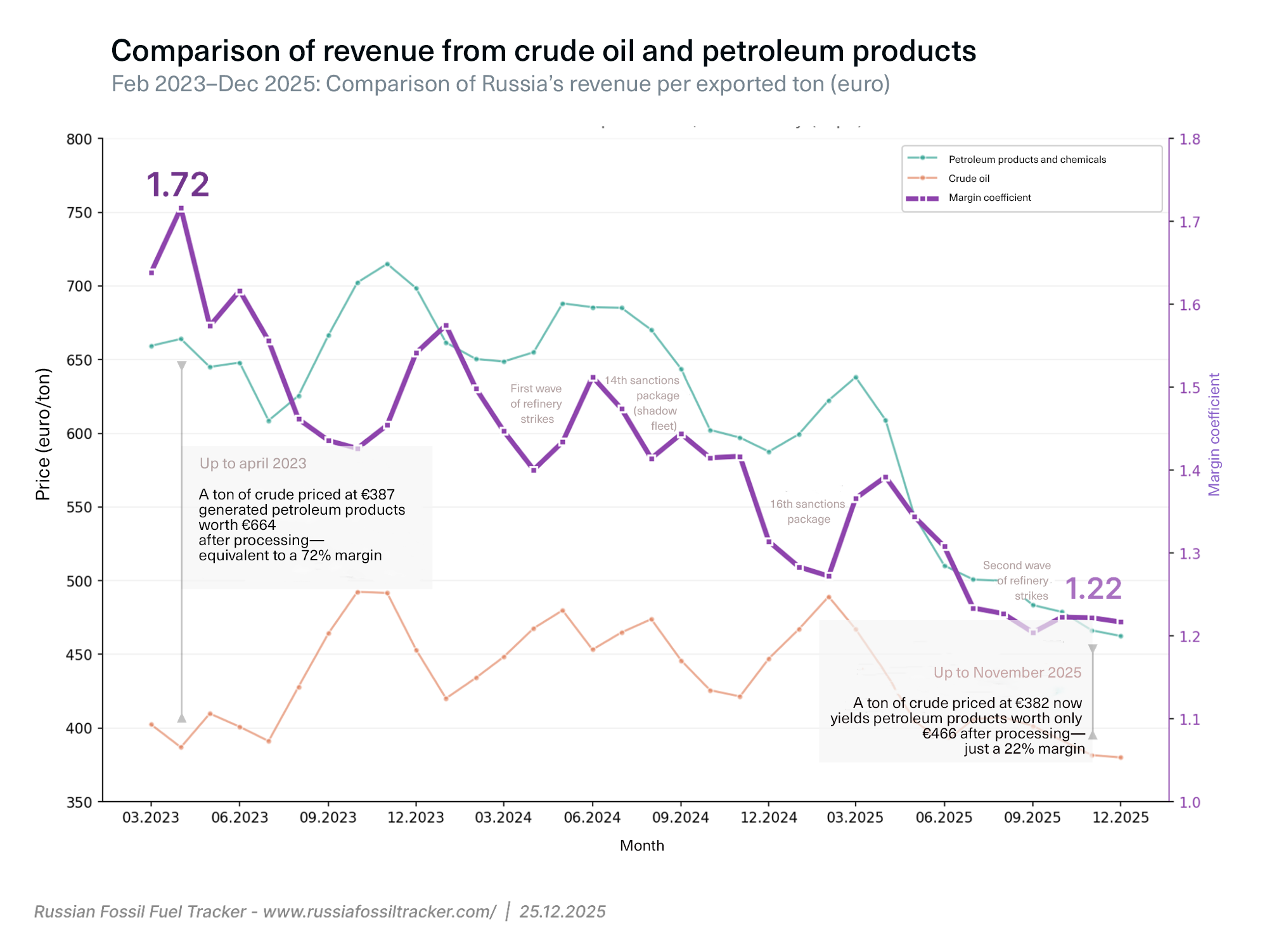

The shift in Russia’s export structure—toward more crude oil and fewer petroleum products, which carry far higher value added—is eroding the profitability of the country’s oil sector.

In April 2023, before Ukraine’s large-scale campaign against refining infrastructure began, the margin coefficient for Russia’s oil exports stood at 1.72. That meant each ton of crude worth €387 generated petroleum products worth €664 after processing—delivering a profit margin of 72%.

By November 2025, that coefficient had collapsed to 1.22. Now a ton of crude worth €382 yields petroleum products worth only €466—just a 22% margin. Profitability has fallen threefold in under two years.

Comparison of revenue from crude oil and petroleum products

Strikes on refineries do not merely cause temporary outages—they physically destroy fixed capital, including high-tech equipment whose import under Western export controls is extremely difficult, if not impossible. Replacing it with Chinese or Russian substitutes takes substantial time and inevitably comes with a significant loss of production efficiency.

Every successful strike on a Russian refinery is not just a few weeks of downtime. It is the gradual accumulation of technological degradation across the entire sector—something that does not show up in quarterly reports but will inevitably shape the real state of Russia’s refining industry three to five years from now.

A political instrument of pressure

Unlike economic sanctions, which generate a slow cumulative effect through the gradual contraction of export markets and rising transaction costs, drone strikes operate on a fundamentally different logic: their political impact can substantially exceed the immediate economic damage.

For the leadership of Russia, the central problem is not so much the current economic losses from damage to individual plants as the uncertainty over how these strikes might escalate in the future. Russia’s energy sector is currently demonstrating the ability to minimize operational impacts from attacks by rerouting production flows and mobilizing spare capacity. But the risk that strikes could escalate to a critical threshold—beyond which existing diversification mechanisms would no longer suffice—is becoming a political factor in its own right.

Notably, the new wave of attacks launched in August 2025 marked the first campaign of this scale under the new U.S. administration of Donald Trump—and its onset coincided with the Alaska summit and a broader breakdown in negotiations over ending the war. In this context, refinery strikes are not so much a tool of gradual economic attrition as a mechanism for shaping a negotiating position—through a visible demonstration of the capacity to inflict unacceptable damage on critical infrastructure.

Conclusion

Ukrainian strikes on Russian refineries will not crash Russia’s economy this year. They will not produce the fuel collapse that stops Russian tanks on the battlefield. Expecting that outcome reflects a fundamental misunderstanding of the nature of this instrument.

But the strikes do something else, no less important. They systematically accelerate the technological degradation of an entire industry already cut off from Western equipment and technology. They steadily compress the margins on the exports that finance the Kremlin’s war machine. They create persistent uncertainty—one that carries a very real political price in any negotiations and fuels social instability through periodic shortages of petroleum products.

In a war of attrition, the winner is ultimately the side that retains the capacity to inflict damage—and absorb it—longer than its opponent. Strikes on refineries are not a “silver bullet” that resolves a conflict in one stroke. They are one tool among many in a comprehensive pressure campaign—whose effectiveness should be measured not by explosions in social-media videos, but by multi-year charts of falling margins.

Photo: depositphotos.com/ua/