Oil prices have slipped below $60 per barrel, adding pressure to a strained Russian economy. At the same time, China—Moscow’s largest trading partner—is locked in a high-stakes tariff war with the United States, triggered by the new U.S. administration. These converging disruptions are unlikely to leave Russia's economic footing - and by extension, its capacity to fund the war in Ukraine—unaffected.

To better understand the current landscape, we once again spoke with Vladimir Milov, former Russian Deputy Minister of Energy and a prominent critic of the Putin regime. An economist and energy expert, Milov was a close ally of opposition leader Alexei Navalny and currently serves as Vice President of the Free Russia Foundation. Our previous conversation with him took place in December 2024. In this latest interview, we revisit his earlier forecasts and examine how recent developments have altered Russia’s economic trajectory.

Question (Q): There’s increasing talk about a potential easing of economic sanctions on Russia—at least from the U.S. While a full rollback seems unlikely, some form of relief may be on the horizon. In your view, could this act as a lifeline for the Kremlin, enabling it to sustain the war effort?

Answer (A): I have written about it in much detail in a recent op-ed for The Insider - please have a look. Long story short - Trump won't be able to reverse Western sanctions policy, and European actions matter more than those of the U.S. Before the 2022 full-scale invasion, Europe was Russia's key investor and trade partner - over 67% of accumulated FDI stock came from Europe and around 50% of Russian exports went to Europe. The U.S. - 1% and 4% respectively. Russia needs markets and investment, and the U.S. won't provide that - even in better times, American investors didn't particularly like Russia.

However, Russia may get some benefits from U.S. sanctions being lifted, which will help to keep Putin's ailing economy afloat for a bit longer. Crucial thing is access to the U.S. technology which may boost the Russian military production - this assessment is shared in a brilliant recent report by the Kyiv School of Economics on the status of the Russian military industries - quite worth a read, I strongly recommend

Another problem is that Europe doesn't have anything comparable to the U.S. global sanctions enforcement mechanism - experienced agencies like the U.S. Office of Foreign Assets Control and Bureau of Industry and Security. If the U.S. lifts sanctions against Russia - or simply continues the crackdown on its own Government institutions like that executed by DOGE - the EU, Britain, and other Western democracies simply don't have its own institutional capacities to secure proper sanctions enforcement on a global scale, as currently provided by the U.S. There will be a major sanctions enforcement vacuum which Putin will inevitably use for his own benefit, boosting sanctions circumvention.

(Q): The U.S.-China tariff war has dominated headlines in recent weeks, signaling historic geopolitical and economic shifts. While Russia isn't directly involved, key trade partners like China are heavily impacted. Beyond oil, should we expect any spillover effects on the Russian economy?

(A): Yes, there's so much more than just oil. China's economic slowdown closed their market for many Russian products, due to which major Russian industries suffer badly. For once, China-oriented Russian coal industry is collapsing right in front of our eyes. Fisheries suffer from contraction of Chinese imports of Russian fish. Russian steelmakers face output contraction and sharply falling profits because cheap Chinese steel is flooding global markets - Chinese economic slowdown turned China from being a major importer to a net exporter of steel. And so on. Russian non-energy and non-commodity exports are down by about a quarter compared to pre-2022 levels, and are not rebounding - China doesn't allow Russia to access its market, and it won't change once Chinese economic growth slows down.

Tariff war will obviously exacerbate Chinese slowdown. The slower Chinese growth - the less market for Russian goods. Share of China in the total Russian exports is as high as a third now - we're heavily dependent on this market and its well-being.

(Q): In a recent interview, you mentioned that further declines in oil prices might actually benefit Russia more than if prices remain stagnant just below a certain threshold—an idea that might seem counterintuitive to many. Could you explain how that works?

(A): Biggest loser from the falling oil prices is not Russia, and not OPEC - its the American shale oil industry. Oil production costs in the U.S. are significantly higher than in Russia or OPEC. This means that, if global oil prices fall below $50, large part of the U.S. oil production will be wiped off the market, and prices will quickly rebound. We already saw these effects after 2014 and 2020 oil price crashes.

Russians know that, which is why they weren't too scared with Trump's threats to "radically bring down the oil prices". Their strategy is to wait out for mass extinction of the U.S. oil production under $50/bbl, and to wait for prices to rebound thereafter. Russian oil producing companies are OK under $30-40 prices - it is the state budget which will suffer, but Putin and his people believe they can last for some time under low oil prices, given that they will be rebounding later.

In these circumstances, I'd say the best scenario if the international oil prices will stay somewhere around $60. Given the sanctions-driven discounts, that means Russian oil cheaper than $50. These are the prices which will significantly hurt Russia (Russian budget is drafted under $70/bbl oil price assumption), but will prevent the collapse of the U.S. shale oil industry and further rebounding of prices. Oil at $50 or cheaper is a much worse scenario, as it will most likely mean that low oil prices will be short-lived, which will make Putin happy.

(Q): During our last conversation, there was an expectation that Russia’s central bank would raise interest rates, yet it held steady at around 21%. What factors led to that unexpected decision?

(A): After their February Board meeting, Central Bank has admitted that "consequences of further raising rates will be worse than keeping the rates steady" - meaning that it would exacerbate economic slowdown or probably lead to a recession. To avoid that, they partially sacrificed the goal of bringing down inflation - which still remains high, preventing the Central Bank from much-anticipated easing of monetary policies. At the recent March meeting of the Central Bank board, only two signals were discussed - neutral and tough (further increasing the rate).

Central Bank faces tough dilemma now - interest rate of 21% is still very high (Russia has 12th highest Central Bank rate in the world), rapidly cooling the economy, but inflation is not really receding. The root causes of inflation - heavy budgetary spending on the war, output gap created by output not catching up with demand due to Western sanctions against Russian manufacturing sector - are not going away. At the same time, Russian industrial output has zeroed out in February (0,2% year-on-year growth and 0,4% seasonally adjusted growth compared to January), and March figures may be even worse - soon we'll see the statistics. So, Central Bank has managed to rapidly cause stagnation with its tight monetary policies - risking further slipping into recession - but it failed to bring inflation under control.

(Q): Your latest FRF Think Tank report points to high inflation and near-zero output growth in Russia—classic signs of stagflation. However, some economists argue that high unemployment is a necessary component. Given that unemployment remains relatively low, does this mean Russia hasn’t yet entered stagflation, or is this just a statistical distortion due to the mass recruitment of the male population?

(A): True, Russian situation is unique. The term "stagflation" was coined in the 1960s and 1970s in the Western economies none of which experienced such a mass diversion of the workforce to the war as Russia today. If the current war is suddenly over, Russia will indeed experience high unemployment - masses of soldiers returning to civilian life won't easily find jobs.

Russia also continues to experience very high hidden unemployment - workforce which is nominally employed, but in reality is either on unpaid leave, part-time workweek, or downtime. Rosstat estimated hidden unemployment to be as high as 4,7 million people in Q4 2024, or over 6% of the total workforce. Together with official unemployment, that would make about 9% of the workforce.

These workers would have significantly eased the pressure on labor market should they have left their enterprises, but Russian labor market traditionally features low mobility (remember how people in the 1990s preferred to continue working for years at enterprises which haven't paid them salaries, instead of leaving them looking for new jobs). So, companies nominally keep the workers, but effectively don't pay them - hoping for recovery, which is not coming (nearly three quarters of hidden unemployment are people on unpaid leave).

So, if we're into a macroeconomic debate by the book here, Russia does have high unemployment - but in hidden or delayed forms. And stagflation is real. If the current situation lingers on, even nominal unemployment will rise quite soon.

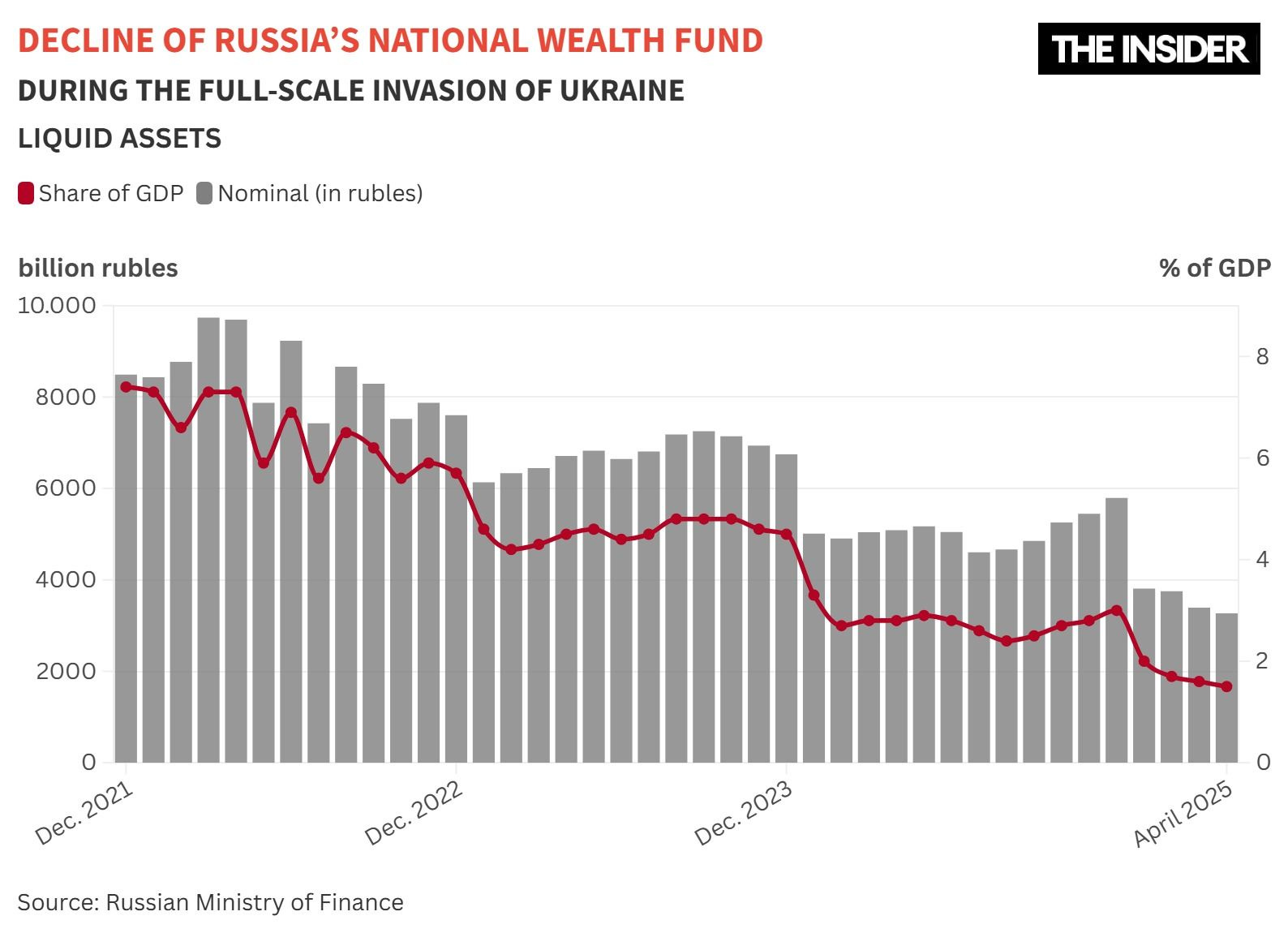

(Q): What is the current situation with Russia's National Wealth Fund — the main financial reserve that has supported Putin's economy through years of war? What are the implications for the Kremlin and the ongoing war?

(A): As of April 1st, the liquidity portion of the National Wealth Fund (NWF) stood at $39 billion, or just over RUR 3 trillion. That's lower than the federal budget deficit recorded in 2024 (RUR 3,5 trillion). As it goes, 2025 budget deficit will likely be much higher - costs are rising (over 20% federal expenditure growth in Q1 2025), while revenues will be depressed by both the falling oil prices, as well as economic slowdown. Already now, non-oil revenue in Q1 2025 grew only by 11% year-on-year, against 26% growth in 2024, and 18% planned growth for 2025. Of which VAT - by just 9%, as opposed to 22% in 2024 and 17% planned for 2025. Slowing economy generates less taxes, which will undermine budget revenues to an extent not lesser than falling oil prices, and lead to further depletion of the NWF. As it looks from today, there's no other way but for the liquidity portion of the NWF to be fully depleted by the end of 2025 (usually they draw the funds from NWF in December to close the fiscal year).

There's also a non-liquidity portion of the NWF, but it largely exists only on paper, with money invested in various securities and not being easily recoverable. For those interested in details, I have analyzed this in my February brief on the Russian economy. The liquidity portion of the NWF has shrank from $116,5 billion in February 2022 to just $39 billion now as a result of heavy war-related spending. Essentially, this was the model of much-praised Putin's "economic resilience": heavily draw the available cash reserves to compensate for the negative effects of sanctions. But this "economic miracle" appears to be over, disappearing along with cash being spent.

What next after the liquidity part of the NWF is fully spent? I also analyze this in one of my recent reports in detail. Bottom line: nothing is working except monetary emission, printing the money. Government can't borrow - they are cut off from international financial markets, and domestically, with yields as high as over 16% for OFZ government bonds, Russia spends more on repaying and servicing the debt than it actually raises from the domestic debt market. Net debt raising was just around zero in 2024 and negative in Q1 2025. They can raise taxes, but that would further undermine economic growth and curb tax base - they'll lose more in the end. Hypothetically, they can try to privatize state assets, but there's not really much to sell if they don't opt to privatize control equity shares in major state companies - and they don't seem to even consider that for strategic reasons. As far as smaller-scale privatization is concerned, it won't solve their fiscal problems on a large scale, and there won't be much demand given the rapid deterioration of investment climate, ongoing rampant nationalization, etc.

So printing the money seems to be the only viable option left. Russian authorities seem to increasingly tolerate high inflation - "we're not Turkey or Argentina yet, so what difference does it make if inflation is 12-13% instead of 10% - let's print a couple of trillion rubles, no one will notice" (that was literally said by some State Duma deputies during Nabiullina's report debate on April 9th). Central Bank clearly shifted to limited emission schemes in the past few months through repo auctions - banks buy government bonds, and are immediately allowed to use them as collateral while borrowing cash from the Central Bank through repo auctions. Central Bank promised to use repo auctions as temporary mechanism in November 2024, but keeps rolling them over - switching from monthly to weekly repo auctions. Effectively, it is little different from Central Bank's credit to the government, or, in simple words, printing the money.

No question that filling the budgetary gap with printed money will lead to even higher inflation, which will destroy any prospect for economic recovery. So, basically, the Western sanctions are working - albeit not as fast as we hoped, but still.

If you found this interview valuable, we invite you to sign up to receive all our analytical reports. You can also support our work by becoming a monthly subscriber — your contributions help us produce more in-depth, independent content like this.

Honest analysis and open discussion rely on editorial independence, and that’s only possible thanks to readers like you.

This Substack is reader-supported. To receive new posts and support my work, consider becoming a free or paid subscriber.